FHA Credit and Your FHA Loan

Take the Steps to Review Your Credit

FHA loan rules apply for all borrowers when it comes to basic minimum credit standards. The FHA loan requirements that will affect your transaction include FICO score rules, down payment requirements, and the basic terms of your mortgage.

You cannot be rejected for an FHA home loan on the basis of factors that have nothing to do with your financial qualifications, employment, income, being an owner/occupier, etc. A home may not be suitable for an FHA loan, a borrower may be denied the loan because he or she doesn't intend to live in the property as the primary residence, or because of factors that affect the economic life of the property.

Credit Requirements for FHA Loans

FHA loans provide great assistance to many first-time homebuyers by offering mortgage loans with lower down payments. While this is a benefit for many people, recent changes in FHA Loan credit requirements may have put the loans just out of reach for some would-be homeowners with questionable credit history.

- The Facts About FHA Credit Requirements and FICO® Scores

- What FICO® Score Do I Need Buy A Home?

- Questions About Credit and Buying a Home

Benefits of Having Good Credit

Homebuyers looking to take advantage of great FHA loan benefits should already know they need to establish the best possible credit rating. FHA loan applicants with a better credit rating increase their options for mortgage or refinance loans.

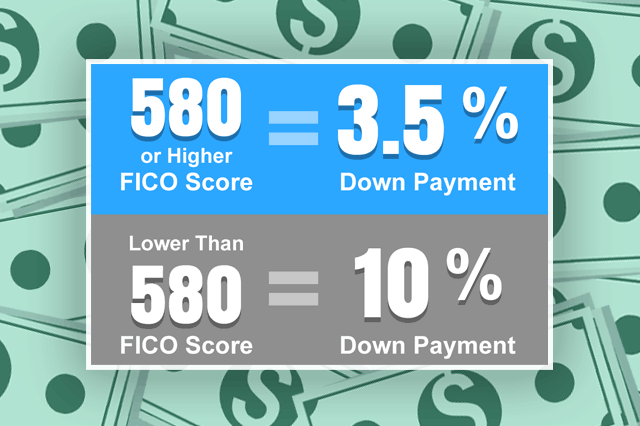

In order to qualify for the low 3.5% FHA loan down payment, applicants will need a FICO® score of at least 580. Those that don't meet that criteria will have to put a down payment of 10% on the mortgage they want.

- Qualifying for a Mortgage: 5 Things to Know

- Facts About Your Credit Scores

- How to Prepare Your Credit for an FHA Home Loan

Improving Your Credit

If your credit is less than solid, consider delaying your home purchase and work on improving their credit scores. Applicants who have a minimum credit score of less than 500 are not eligible for FHA mortgages.

While FHA loans are a great option for people buying a house, applicants can make the process even easier if they take steps toward ensuring their credit history is in tip-top shape. FHA advises prospective homebuyers to approach the loan process with their best possible credit history to eliminate any potential risk of not qualifying.

- FHA Loans, Missed Payments, and My Credit Report

- Minimum Credit Scores for FHA Loans

- Ways to Improve Your Credit Ahead of Your Home Loan

Fixing Credit Report Errors

Some borrowers who want to apply for an FHA loan find their applications held up by problems with what is on their credit report. Take proper steps to check the accuracy of your credit report with Experian®, TransUnion® and Equifax®.

Once you've gotten your report from the three bureaus, carefully examine your credit history for anything out of the ordinary, such as unauthorized loans taken out in your name, incorrect late payment records or anything that seems questionable, no matter how minor you think it is.

- Credit Monitoring, Data Security Breaches, and Your FHA Loan

- The Facts About FHA Credit Requirements and FICO Scores

- FHA Home Loan Applications and Credit Freeze Issues

Identity Theft and Fraud in the News

Now more than ever, it is crucial to pay close attention to your credit reports due to elevated security breaches, hacks, and security compromises. No major corporation is immune to these attacks-including the credit reporting agencies themselves.

We've listed a timeline of some of the most headline-grabbing hacks reported in recent years. Remember, these are only SOME of the incidents you may have heard about; each one is a good example of why it pays to continuously monitor your credit.

- FHA Home Loan Applications and Credit Freeze Issues

- Credit Monitoring, Data Security Breaches, and Your FHA Loan

- Credit Advice for Home Loan Applicants

SEE YOUR CREDIT SCORES From All 3 Bureaus

Do you know what's on your credit report?

Learn what your score means.

FHA Loan Articles and Mortgage News

July 26, 2024 - The FHA 203(k) rehabilitation mortgage and its refinance equivalent are tools for buying and renovating a home or remodeling an existing property. This loan can be used to buy a fixer-upper and finance the repairs needed to make the home livable and meet local building codes.

July 25, 2024 - The U.S. Department of Housing and Urban Development issued a proposed new rule in July 2024 that is intended to be a permanent policy regarding the sale of delinquent FHA single-family mortgage loans.

July 23, 2024 - When shopping for a home loan, you need to gather some basic information from multiple lenders to compare the costs, fees, terms, and conditions of the home loan you seek. During this process, you can verify information with each lender you choose.

July 22, 2024 - As we age, the significance of making sound financial decisions grows. Many choose to tap into their home equity in their retirement years, and two options are important to know: FHA reverse mortgages and FHA refinancing.

July 21, 2024 - FHA refinancing is worth considering if you want a government-backed loan insured by the Federal Housing Administration (FHA) that can refinance you out of a conventional adjustable rate mortgage or get you cash back at closing.