FHA Requirements

Debt-to-Income Ratio Guidelines

In order to prevent homebuyers from getting into a home they cannot afford, FHA requirements and guidelines have been set in place requiring borrowers and/or their spouse to qualify according to set debt to income ratios. These ratios are used to calculate whether or not the potential borrower is in a financial position that would allow them to meet the demands that are often included in owning a home.

The two ratios are as follows:

1) Mortgage Payment Expense to Effective Income

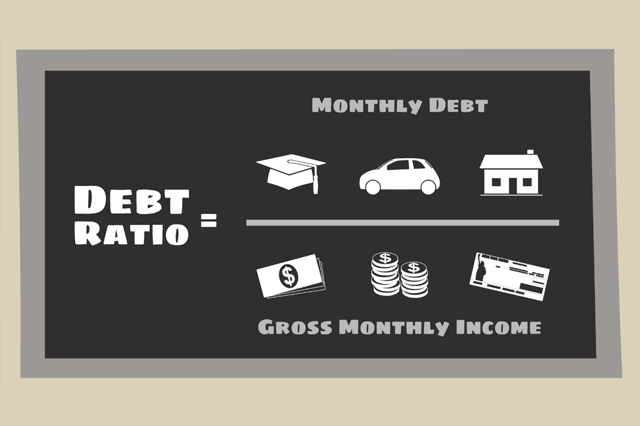

Add up the total mortgage payment (principal and interest, escrow deposits for taxes, hazard insurance, mortgage insurance premium, homeowners' dues, etc.). Then, take that amount and divide it by the gross monthly income. The maximum ratio to qualify is 31%.

See the following example:

2) Total Fixed Payment to Effective Income

Add up the total mortgage payment (principal and interest, escrow deposits for taxes, hazard insurance, mortgage insurance premium, homeowners' dues, etc.) and all recurring monthly revolving and installment debt (car loans, personal loans, student loans, credit cards, etc.). Then, take that amount and divide it by the gross monthly income. The maximum ratio to qualify is 43%.

See the following example:

Please note that the above indicators do not exclusively determine whether or not a candidate will qualify for an FHA loan. Other factors will be considered, including credit history and job stability.

FHA Loan Requirements

SEE YOUR CREDIT SCORES From All 3 Bureaus

Do you know what's on your credit report?

Learn what your score means.

FHA Loan Articles and Mortgage News

July 26, 2024 - The FHA 203(k) rehabilitation mortgage and its refinance equivalent are tools for buying and renovating a home or remodeling an existing property. This loan can be used to buy a fixer-upper and finance the repairs needed to make the home livable and meet local building codes.

July 25, 2024 - The U.S. Department of Housing and Urban Development issued a proposed new rule in July 2024 that is intended to be a permanent policy regarding the sale of delinquent FHA single-family mortgage loans.

July 23, 2024 - When shopping for a home loan, you need to gather some basic information from multiple lenders to compare the costs, fees, terms, and conditions of the home loan you seek. During this process, you can verify information with each lender you choose.

July 22, 2024 - As we age, the significance of making sound financial decisions grows. Many choose to tap into their home equity in their retirement years, and two options are important to know: FHA reverse mortgages and FHA refinancing.

July 21, 2024 - FHA refinancing is worth considering if you want a government-backed loan insured by the Federal Housing Administration (FHA) that can refinance you out of a conventional adjustable rate mortgage or get you cash back at closing.