FHA Loan Tips for Improving Credit

Track Your Credit Score and Stay on Top of Problems

While FHA loans are known as a great service for people looking for help buying a house, applicants can make the process even easier if they take steps toward ensuring their credit history is in tip-top shape. The agency advises prospective homebuyers to approach FHA loans with their best possible credit history to eliminate any potential risk of not qualifying.

Whether you're looking for a loan to mortgage a new house or to refinance a house you already own, it makes the most sense open up all your options with an optimal credit rating. The FHA recommends having a satisfactory payment history of at least one year before applying for a loan.

Credit Tips for Your FHA Loan

Here are some tips to help you on your way:

- Take a Close Look at Your Credit Reports

You don't know what could be hurting your credit score unless you actually check. Get your credit reports from the three national credit bureaus--Experian, Equifax and TransUnion--at no cost and comb them over for anything suspicious or questionable. - Dispute Inaccuracies

If you find errors on your credit report, notify the reporting bureau in writing so you have a record. Provide any additional records or evidence you have to support your dispute. - Find Professional Help

The FHA recommends applicants with credit problems get help from a Consumer Credit Counseling program. A credit counselor can help you get back on track. - Bankruptcy / Foreclosure

If you've suffered from a bankruptcy or foreclosure in the past few years, you might still be able to qualify for an FHA loan. Develop a satisfactory payment history, re-establish good credit and meet the other FHA requirements.

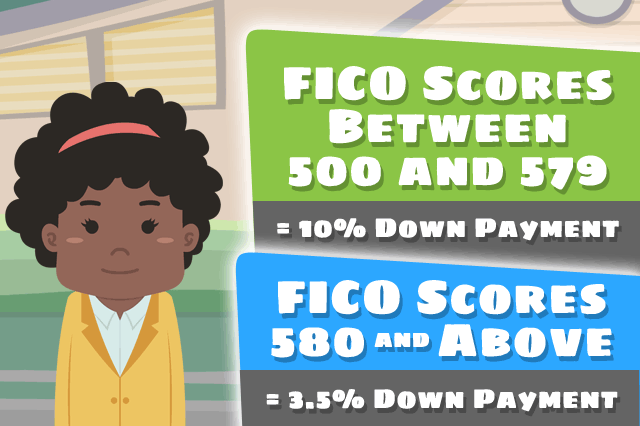

While your credit history is just one of the many factors that make up your eligibility for an FHA loan, it is no doubt one of the most important. Having a higher score not only helps you qualify, you can also benefit from the low 3.5 percent down payment on mortgage loans available to applicants with a FICO score over 580. FHA approved lenders don't take your credit history lightly, and neither should you.

Credit Scores for FHA Loans

SEE YOUR CREDIT SCORES From All 3 Bureaus

Do you know what's on your credit report?

Learn what your score means.

FHA Loan Articles and Mortgage News

July 11, 2024 - Appraisals and home inspections are two separate but very important processes. For the purpose of this article, we focus on the mandatory FHA appraisal process the lender uses to establish the fair market value of the home.

July 9, 2024 - The FHA Home Equity Conversion Mortgage (HECM) loan program is an option for qualifying borrowers 62 or older. These loans require no monthly payment and feature a cash out option for the borrower.

July 8, 2024 - The FHA loan FICO score requirement is easy to understand. If your FICO scores fall between 500 and 579, FHA loan rules say you must pay 10% down, assuming lender standards allow loan approval for those scores.

July 6, 2024 - The FHA single-family home loan program includes both a fixed-interest rate option and an adjustable-rate home loan (ARM). In a housing market where mortgage rates are higher than they have been in many years, the adjustable-rate FHA loan is an option many consider.

July 3, 2024 - Borrowers sometimes assume things about home loan programs that aren’t true. For example, the USDA home loan option requires that the homes purchased with such loans must be in a rural area. But the USDA’s definition of rural is often quite different than you might think.