Compare Your Options for Your New Home Loan

December 19, 2021

Some wonder if it’s worth the effort to shop around for a home loan. There’s a misconception you might suffer from at the beginning of your home loan journey that all lenders are alike. But the reality is that you may find important differences among FHA lenders in several ways--the types of loan on offer and other issues.

Comparing lenders is always a good idea. Borrowers who think they have made up their minds already and choose to continue using their long-term lender to get the new loan or refinance might not have all the information they need to make a truly informed choice.

Do you know how other potential lenders structure their fees, closing costs, and rates? How competitive are they with the lender you know? Are you sure you can’t find a better deal?

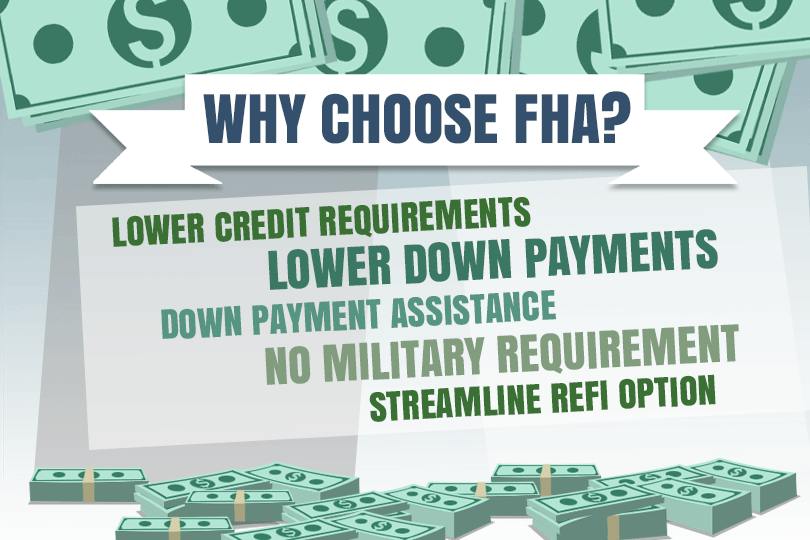

FHA home loan fees and expenses are regulated, it is true--the amount you can be charged, the kinds of costs you cannot be made responsible for, the amount of your minimum required down payment, etc.

Some new to the house hunting process don’t know (at first) that FHA loan guidelines are not the only ones at work in the calculation of costs of the loan. Your lender may have higher minimum standards and other requirements. These may vary more among companies than you realize.

And then there are the kinds of loans themselves. Do you want a manufactured home? A condo? A suburban house? Not all banks that offer FHA mortgages will offer those loans specifically, so it’s smart to ask upfront.

And some banks handle their interest rates and closing costs differently. Some, when rates are rising, will choose not to adjust the mortgage rate. They may choose to alter closing costs instead.

This is a common practice, not a scam, and it reflects that financial institution’s policy toward reacting to the latest changes in rates. Some will simply make the corrections. Others may change the closing costs instead. Does it affect you? It may, especially if you have chosen to pay the closing costs upfront rather than financing the ones your loan officer allows you to.

When you compare lenders, don’t neglect to ask about BOTH rates and costs--these two sets of numbers from every lender you speak with can help you decide which one to choose OR which one to approach with more competitive rates with an eye on negotiating a better deal.

Some are intimidated by the idea of haggling over these things. Those who need to save money upfront, reducing out-of-pocket costs tend to feel a bit more emboldened than others. It may be necessary to get used to the idea of negotiating but doing so may help you save that money and get you a more competitive mortgage offer.

And that makes the discomfort of haggling compete with the need to save money on the transaction.

------------------------------

RELATED VIDEOS:

Do What You Can to Avoid Foreclosure

Homes Financed With FHA Loans Must Be Owner Occupied

FHA Programs for First-Time Homebuyers

Comparing lenders is always a good idea. Borrowers who think they have made up their minds already and choose to continue using their long-term lender to get the new loan or refinance might not have all the information they need to make a truly informed choice.

Do you know how other potential lenders structure their fees, closing costs, and rates? How competitive are they with the lender you know? Are you sure you can’t find a better deal?

FHA home loan fees and expenses are regulated, it is true--the amount you can be charged, the kinds of costs you cannot be made responsible for, the amount of your minimum required down payment, etc.

Some new to the house hunting process don’t know (at first) that FHA loan guidelines are not the only ones at work in the calculation of costs of the loan. Your lender may have higher minimum standards and other requirements. These may vary more among companies than you realize.

And then there are the kinds of loans themselves. Do you want a manufactured home? A condo? A suburban house? Not all banks that offer FHA mortgages will offer those loans specifically, so it’s smart to ask upfront.

And some banks handle their interest rates and closing costs differently. Some, when rates are rising, will choose not to adjust the mortgage rate. They may choose to alter closing costs instead.

This is a common practice, not a scam, and it reflects that financial institution’s policy toward reacting to the latest changes in rates. Some will simply make the corrections. Others may change the closing costs instead. Does it affect you? It may, especially if you have chosen to pay the closing costs upfront rather than financing the ones your loan officer allows you to.

When you compare lenders, don’t neglect to ask about BOTH rates and costs--these two sets of numbers from every lender you speak with can help you decide which one to choose OR which one to approach with more competitive rates with an eye on negotiating a better deal.

Some are intimidated by the idea of haggling over these things. Those who need to save money upfront, reducing out-of-pocket costs tend to feel a bit more emboldened than others. It may be necessary to get used to the idea of negotiating but doing so may help you save that money and get you a more competitive mortgage offer.

And that makes the discomfort of haggling compete with the need to save money on the transaction.

------------------------------

RELATED VIDEOS:

Do What You Can to Avoid Foreclosure

Homes Financed With FHA Loans Must Be Owner Occupied

FHA Programs for First-Time Homebuyers

Do you know what's on your credit report?

Learn what your score means.