FICO Scores and Home Loans: What You Need to Know

June 22, 2021

Are you ready to apply for a home loan? You might FEEL ready, but there are certain steps you should take ahead of filling out any loan application. What kind of steps? One of the most important is asking yourself how long it’s been since you reviewed your credit report.

If you don’t know the contents of your credit report, you aren’t ready to apply for a mortgage loan, an auto loan, or even a personal line of credit. Why? Because your lender will review not only your FICO score, but your credit activity for a minimum of the last 12 months leading up to your loan application.

If you don’t know what the lender will see, you just aren’t ready to apply.

Multiple Credit Reports

There are three major credit reporting agencies, Equifax, TransUnion, and Experian. You will need to know what all three credit reporting agencies say about you in your credit report.

Why? One credit report may contain errors or other problems the others do not reflect. Not all credit reports update at the same time.

And it does not help to simply check your credit score.

FICO Scores Count, But So Does Your Credit Use

FICO scores are crucial for FHA loan approval, and borrowers should respect FICO scores and the factors that change them. But those credit scores aren't capable of telling the lender your whole financial story--at least where the last 12 to 24 months are concerned.

Your record of payments on financial obligations are just as important as the scores. If you have late or missed payments 12 months leading up to your loan application, you are at a serious disadvantage.

FICO scores are also a big part of what the lender will decide regarding your down payment.

FHA FICO Score Rules

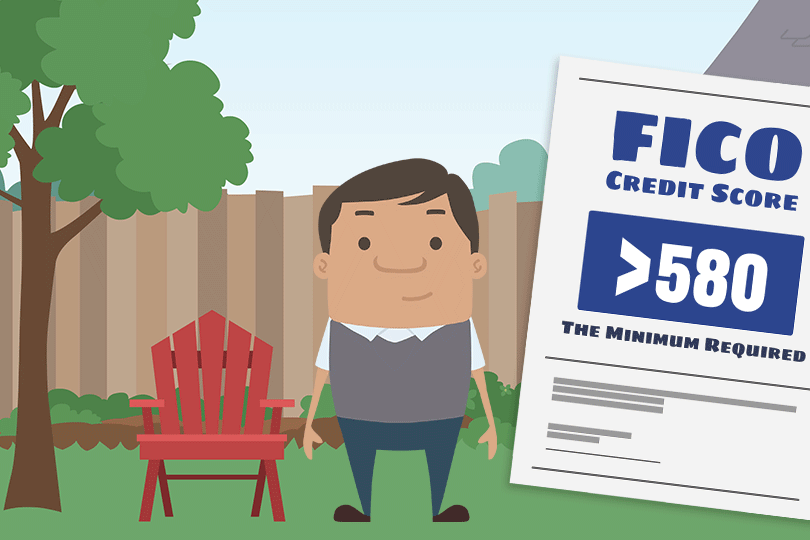

FHA single-family home loan rules include a set of FICO scores that allows you qualify for FHA maximum financing and the lowest (3.5%) down payment. On paper in the FHA loan rulebook, that credit score range is 580 or better.

Borrowers with FICO scores below 580, but not lower than 500 do technically qualify for an FHA loan but must provide a minimum of 10% down. Lender standards will apply and your experience may vary depending on circumstances. But as a general rule of thumb, these are numbers to pay attention to.

Find out what your FICO scores are from the three major credit reporting agencies, and also learn what participating lenders will expect for approving low down payments on your mortgage.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

If you don’t know the contents of your credit report, you aren’t ready to apply for a mortgage loan, an auto loan, or even a personal line of credit. Why? Because your lender will review not only your FICO score, but your credit activity for a minimum of the last 12 months leading up to your loan application.

If you don’t know what the lender will see, you just aren’t ready to apply.

Multiple Credit Reports

There are three major credit reporting agencies, Equifax, TransUnion, and Experian. You will need to know what all three credit reporting agencies say about you in your credit report.

Why? One credit report may contain errors or other problems the others do not reflect. Not all credit reports update at the same time.

And it does not help to simply check your credit score.

FICO Scores Count, But So Does Your Credit Use

FICO scores are crucial for FHA loan approval, and borrowers should respect FICO scores and the factors that change them. But those credit scores aren't capable of telling the lender your whole financial story--at least where the last 12 to 24 months are concerned.

Your record of payments on financial obligations are just as important as the scores. If you have late or missed payments 12 months leading up to your loan application, you are at a serious disadvantage.

FICO scores are also a big part of what the lender will decide regarding your down payment.

FHA FICO Score Rules

FHA single-family home loan rules include a set of FICO scores that allows you qualify for FHA maximum financing and the lowest (3.5%) down payment. On paper in the FHA loan rulebook, that credit score range is 580 or better.

Borrowers with FICO scores below 580, but not lower than 500 do technically qualify for an FHA loan but must provide a minimum of 10% down. Lender standards will apply and your experience may vary depending on circumstances. But as a general rule of thumb, these are numbers to pay attention to.

Find out what your FICO scores are from the three major credit reporting agencies, and also learn what participating lenders will expect for approving low down payments on your mortgage.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

Do you know what's on your credit report?

Learn what your score means.