Credit Repair Hacks for FHA Loan Applicants

December 10, 2020

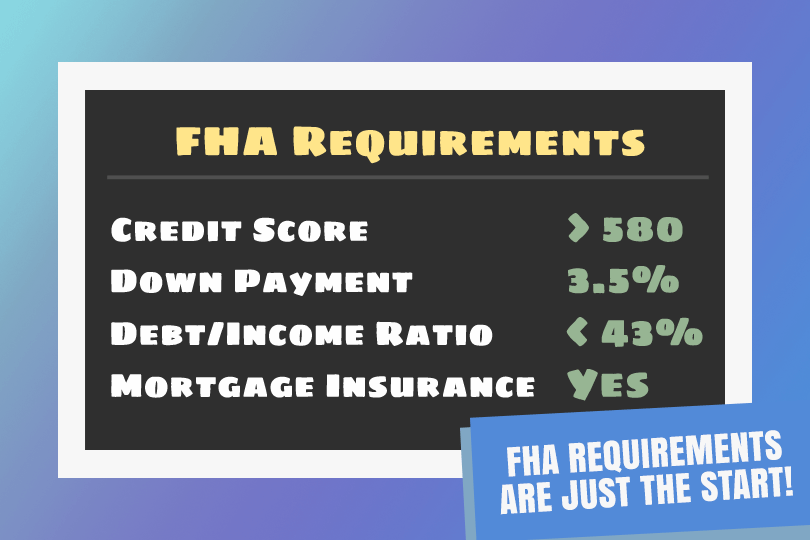

Lots of people want to know if there are credit repair hacks they can try ahead of applying for a home loan. Are you worried about your credit? Afraid an FHA lender won’t approve your home loan because of your FICO score or credit history?

There are four credit repair hacks you can do ahead of your home loan. The key to getting these hacks right is to start as early as possible--at least one year--ahead of your home loan application. It’s never too late to start repairing your credit.

How to Get Started Repairing Your Credit

The number one credit repair hack? Knowing your credit report, and knowing it well. It's that simple, really. No, you won’t be able to repair your credit just by knowing what’s in your credit report. But credit score literacy is an important tool you’ll need to accomplice the other credit hacks below.

Knowing your credit report well is only the first step. Those who follow through and begin monitoring their credit on a regular basis go a long way toward a “no surprise” situation when your lender opens the report to justify approving your home loan.

Actively monitoring your credit means using a service to provide you with early warnings about potential identity theft, changes in your FICO score, etc.

It’s vital to remember you will want to resolve such issues long before applying for your home loan. Anything less risks you getting turned down. Keep in mind that credit reports don’t update instantaneously and any changes to your credit report as a result of a dispute will take time to update across the credit reporting agencies. Nothing is overnight or instantaneous when it comes to credit.

Pay on Time, Cut Your Existing Debt

At LEAST a year ahead of time, make a budget that will let you pay ALL your bills on time. You will also want to begin cutting down revolving debt balances. Don’t close your revolving credit accounts (see below) but do pay them down as much as possible. Why?

The lower your total amount of monthly debt, the better your chances at home loan approval. Credit mistakes like late or missed payments 12 months before your mortgage loan application make it harder for your lender to label you as a good credit risk.

Don't Apply for New Credit

Any complications associated with your current debt-to-income ratio or situations that add more debt make it much harder for your loan officer to justify approving your mortgage. Help your lender help you by avoiding new credit until after your home loan has closed and you accept the keys to your new home.

------------------------------

RELATED VIDEOS:

There's a Difference Between APR and Interest Rates

Choose Your Mortgage Lender Carefully

Getting Started With Your FHA Loan Application

There are four credit repair hacks you can do ahead of your home loan. The key to getting these hacks right is to start as early as possible--at least one year--ahead of your home loan application. It’s never too late to start repairing your credit.

How to Get Started Repairing Your Credit

The number one credit repair hack? Knowing your credit report, and knowing it well. It's that simple, really. No, you won’t be able to repair your credit just by knowing what’s in your credit report. But credit score literacy is an important tool you’ll need to accomplice the other credit hacks below.

Knowing your credit report well is only the first step. Those who follow through and begin monitoring their credit on a regular basis go a long way toward a “no surprise” situation when your lender opens the report to justify approving your home loan.

Actively monitoring your credit means using a service to provide you with early warnings about potential identity theft, changes in your FICO score, etc.

It’s vital to remember you will want to resolve such issues long before applying for your home loan. Anything less risks you getting turned down. Keep in mind that credit reports don’t update instantaneously and any changes to your credit report as a result of a dispute will take time to update across the credit reporting agencies. Nothing is overnight or instantaneous when it comes to credit.

Pay on Time, Cut Your Existing Debt

At LEAST a year ahead of time, make a budget that will let you pay ALL your bills on time. You will also want to begin cutting down revolving debt balances. Don’t close your revolving credit accounts (see below) but do pay them down as much as possible. Why?

The lower your total amount of monthly debt, the better your chances at home loan approval. Credit mistakes like late or missed payments 12 months before your mortgage loan application make it harder for your lender to label you as a good credit risk.

Don't Apply for New Credit

Any complications associated with your current debt-to-income ratio or situations that add more debt make it much harder for your loan officer to justify approving your mortgage. Help your lender help you by avoiding new credit until after your home loan has closed and you accept the keys to your new home.

------------------------------

RELATED VIDEOS:

There's a Difference Between APR and Interest Rates

Choose Your Mortgage Lender Carefully

Getting Started With Your FHA Loan Application

Do you know what's on your credit report?

Learn what your score means.