First-Time Homebuyers

Know the Basics and Improve Your FHA Loan Chances

As a first-time homebuyer, there might be a lot of unknowns. Whether it's the mortgage lingo, type of home loans, or even down payment requirements, the flood of new information can be overwhelming. We want to help you learn about few of the things that can slip under the radar as you're getting ready to buy your new home.

Grants for First-Time Homebuyers

Grants and specialized loan programs for first-time homebuyers are available in cities and counties throughout the United States. These programs provide down payment and/or closing cost assistance in a variety of forms, including grants, zero-interest loans, and deferred payment loans.

Minimum down payments are generally required. Guidelines usually cover how long a homebuyer must live in the home, where the home is located, where the homebuyer currently lives or works, and the maximum amount of household income for the applicant.

Know Your Credit Score

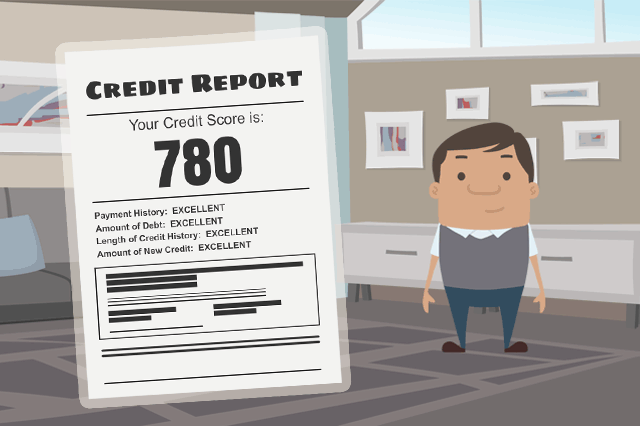

One of the biggest surprises that many first-time homebuyers face is a low credit score. This can happen for a lot of reasons. You may have forgotten to pay your credit card bill for a while. Maybe you never signed up for a credit card, which could mean you don't have an established credit history. There's also the rare chance that you suffered from identity theft that drastically lowered your credit score.

Regardless of the reason, a low credit score can mean a larger down payment requirement or a higher interest rate for a homebuyer. That's why it's best to stay in the know, and monitor your FICO score so you're not faced with any unpleasant surprises. If you're concerned about your credit ranking, here are a few steps you can take:

- Review your credit report. If you know what's in it, you don't have to waste time and energy with guess work. Check to see if there are any errors, and if so, dispute them.

- Pay your bills with a credit card. Set up utility bill payments through a credit card account in your name to help establish credit.

- Pay on time! Missed or late payments can stay on your record for years, making lenders feel that granting you a mortgage could be a risk.

Do you know what's on your credit report?

Learn what your score means.

- FHA Loan Approval: What's in Your Credit Report?

- FHA Loans, Missed Payments, and My Credit Report

- Home Loan Approval, Credit Issues, and Credit Repair

Down Payment Assistance Grants

The down payment is the initial “upfront” payment you make when buying a home. It is seen as your investment in the mortgage, since you stand to lose it if you default on the monthly payments that come after. While many conventional loans require a down payments as high as 20 percent of the total purchase price, FHA loans make things a little easier by requiring 3.5 percent down.

Either way, saving for a hefty down payment on a home can be a burden, so it's a smart move to look for available assistance that will help lessen some of that cost. Many state and local government agencies offer assistance programs such as Down Payment Grants to eligible, first-time homebuyers in order to help them meet down payment and closing cost requirements.

Make sure to take advantage of any Down Payment Assistance Programs offered by your county, municipality, or state to help lower your upfront mortgage costs. Find a Down Payment Assistance Program in your area.

- Types of Down Payment Assistance

- Chenoa Fund Provides Down Payment Assistance Nationwide

- Five Important Down Payment Assistance Tips

FHA Loans for First-Time Homebuyers

FHA loans benefit those who would like to purchase a home but haven't been able to put money away for the purchase, like recent college graduates, newlyweds, or people who are still trying to complete their education. It also allows individuals to qualify for a FHA loan whose credit has been marred by bankruptcy or foreclosure.

This loan often works well for first-time homebuyers because it allows individuals to finance up to 96.5 percent of their home loan which helps to keep down payments and closing costs at a minimum. The 203(b) home loan is also the only loan in which 100 percent of the closing costs can be a gift from a relative, non-profit, or government agency.

- Buying Your First Home With an FHA Mortgage

- Five Things to Remember About FHA Loans

- Housing Counseling for First-Time Home Buyers

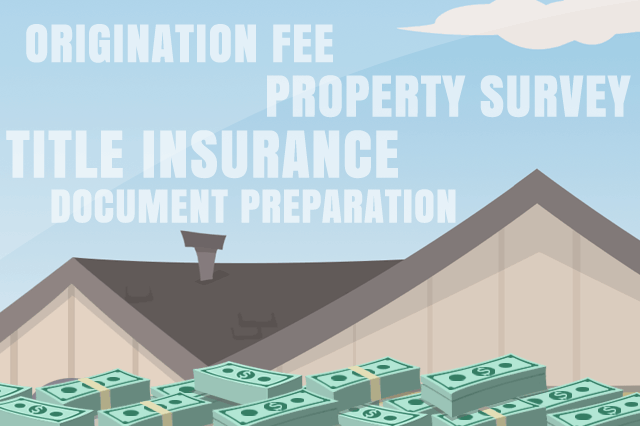

Learn About FHA Closing Costs

Many first-time homebuyers are surprised that the down payment isn't the only thing they're saving up for. There are some upfront costs required to close your mortgage, which can be significant, usually running between 2 and 5 percent of the total loan amount.

When shopping for a home loan, remember to compare prices for certain closing expenses, such as homeowners insurance, home inspections and title searches. In some cases, you may even be able to cut down on closing costs by asking the seller to pay for a portion of them (known as seller concessions) or negotiating your real estate agent's commission. Some of the common closing costs that go into an FHA mortgage include:

- Lender's origination fee

- Deposit verification fees

- Attorney's fees

- The appraisal and any inspection fees

- Cost of title insurance and title examination

- Document preparation (by a third party)

- Property survey

- Credit reports

- Five Facts About Home Loan Closing Costs

- Different Ways to Pay Your Closing Costs

- Prepare for Your Home Loan Application

2024 FHA Loan Limits

The FHA has calculated the maximum loan amounts that it will insure for different parts of the country. These are collectively known as the FHA lending limits. These loan limits are calculated and updated annually. They're influenced by type of home, such as single-family or duplex, and location. Some homebuyers choose to purchase homes in counties where lending limits are higher, or may look for homes that fit within the limits of the place they want to live.

| LOW COST AREA | |||

| 2024 FHA Limits | |||

| Single | Duplex | Tri-plex | Four-plex |

|---|---|---|---|

| $420,680 | $538,650 | $651,050 | $809,150 |

| HIGH COST AREA | |||

| 2024 FHA Limits | |||

| Single | Duplex | Tri-plex | Four-plex |

|---|---|---|---|

| $970,800 | $1,243,050 | $1,502,475 | $1,867,275 |

- Learning the Basics About FHA Loan Limits

- When Do FHA Loan Limits Change?

- FHA Loan Limits Facts and Calculations

MIP Is Your Mortgage Insurance Premium

Insurance on FHA mortgages are often rolled into the total monthly payment at 0.55 percent of the total loan amount which is roughly half of the price of mortgage insurance on a conventional loan. FHA will collect the annual MIP, which is the time on which you will pay for FHA Mortgage Insurance Premiums on your FHA loan.

MIP Rates for FHA Loans Over 15 Years

If you take out a typical 30-year mortgage or anything greater than 15 years, your annual mortgage insurance premium will be as follows:

| Base Loan Amount | LTV | Annual MIP |

|---|---|---|

| ≤ $625,500 | ≤ 95% | 80 bps (0.80%) |

| ≤ $625,500 | > 95% | 85 bps (0.85%) |

| >$625,500 | ≤ 95% | 100 bps (1.00%) |

| > $625,500 | > 95% | 105 bps (1.05%) |

- FHA Loans and Mortgage Insurance Requirements

- What You Need to Know About the FHA Mortgage Insurance Premium

- Can I Include UFMIP in My FHA Loan?