FHA Requirements

Debt-to-Income Ratio Guidelines

In order to prevent homebuyers from getting into a home they cannot afford, FHA requirements and guidelines have been set in place requiring borrowers and/or their spouse to qualify according to set debt to income ratios. These ratios are used to calculate whether or not the potential borrower is in a financial position that would allow them to meet the demands that are often included in owning a home.

The two ratios are as follows:

1) Mortgage Payment Expense to Effective Income

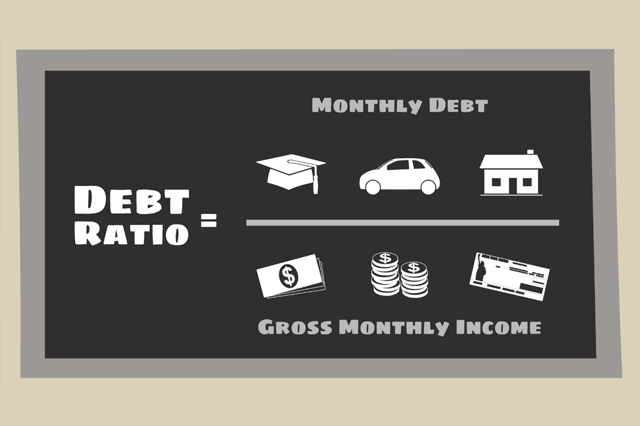

Add up the total mortgage payment (principal and interest, escrow deposits for taxes, hazard insurance, mortgage insurance premium, homeowners' dues, etc.). Then, take that amount and divide it by the gross monthly income. The maximum ratio to qualify is 31%.

See the following example:

2) Total Fixed Payment to Effective Income

Add up the total mortgage payment (principal and interest, escrow deposits for taxes, hazard insurance, mortgage insurance premium, homeowners' dues, etc.) and all recurring monthly revolving and installment debt (car loans, personal loans, student loans, credit cards, etc.). Then, take that amount and divide it by the gross monthly income. The maximum ratio to qualify is 43%.

See the following example:

Please note that the above indicators do not exclusively determine whether or not a candidate will qualify for an FHA loan. Other factors will be considered, including credit history and job stability.

FHA Loan Requirements

SEE YOUR CREDIT SCORES From All 3 Bureaus

Do you know what's on your credit report?

Learn what your score means.

FHA Loan Articles and Mortgage News

May 16, 2024 - You’ve saved your down payment funds, researched the housing market, and worked on your credit. When you apply to be pre-approved or prequalified for an FHA mortgage, there are a few things to review before you start filling out the forms.

May 12, 2024 - The FHA and HUD have revised appraisal rules for FHA single-family loans. The revisions are meant to address issues including housing discrimination at the appraisal level, and provide home buyers with clarified guidelines to contest an appraisal or request a reconsideration of value (ROV).

May 11, 2024 - FHA home loans are just one way to buy a home. Some borrowers pay in cash, some use conventional mortgages, and some qualify for VA home loans. But what do all of these have in common in many cases? The need to use home loan earnest money as part of the transaction.

May 10, 2024 - Which services are required for FHA loans, and which ones are optional? Some borrowers ask this in the planning stages because they’re trying to find ways to stretch their home loan budgets for closing costs and the down payment. We examine some critical services in this article.

May 8, 2024 - You cannot make a down payment or pay closing costs with cold, hard cash. You must render payment in the manner acceptable to the lender, which is typically a wire transfer or some other pre-arranged procedure for down payment money.