FHA Loan Tips for Improving Credit

Track Your Credit Score and Stay on Top of Problems

While FHA loans are known as a great service for people looking for help buying a house, applicants can make the process even easier if they take steps toward ensuring their credit history is in tip-top shape. The agency advises prospective homebuyers to approach FHA loans with their best possible credit history to eliminate any potential risk of not qualifying.

Whether you're looking for a loan to mortgage a new house or to refinance a house you already own, it makes the most sense open up all your options with an optimal credit rating. The FHA recommends having a satisfactory payment history of at least one year before applying for a loan.

Credit Tips for Your FHA Loan

Here are some tips to help you on your way:

- Take a Close Look at Your Credit Reports

You don't know what could be hurting your credit score unless you actually check. Get your credit reports from the three national credit bureaus--Experian, Equifax and TransUnion--at no cost and comb them over for anything suspicious or questionable. - Dispute Inaccuracies

If you find errors on your credit report, notify the reporting bureau in writing so you have a record. Provide any additional records or evidence you have to support your dispute. - Find Professional Help

The FHA recommends applicants with credit problems get help from a Consumer Credit Counseling program. A credit counselor can help you get back on track. - Bankruptcy / Foreclosure

If you've suffered from a bankruptcy or foreclosure in the past few years, you might still be able to qualify for an FHA loan. Develop a satisfactory payment history, re-establish good credit and meet the other FHA requirements.

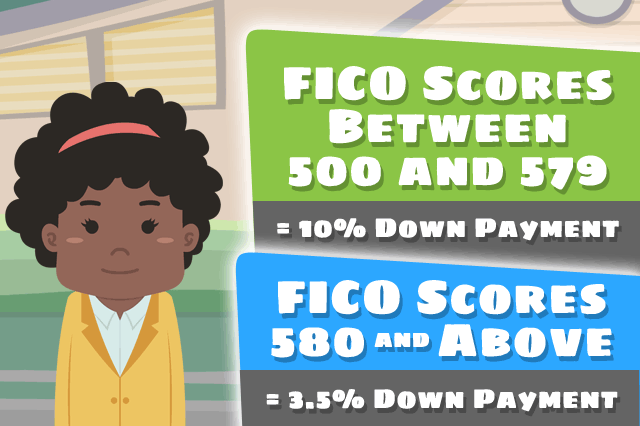

While your credit history is just one of the many factors that make up your eligibility for an FHA loan, it is no doubt one of the most important. Having a higher score not only helps you qualify, you can also benefit from the low 3.5 percent down payment on mortgage loans available to applicants with a FICO score over 580. FHA approved lenders don't take your credit history lightly, and neither should you.

Credit Scores for FHA Loans

SEE YOUR CREDIT SCORES From All 3 Bureaus

Do you know what's on your credit report?

Learn what your score means.

FHA Loan Articles and Mortgage News

May 16, 2024 - You’ve saved your down payment funds, researched the housing market, and worked on your credit. When you apply to be pre-approved or prequalified for an FHA mortgage, there are a few things to review before you start filling out the forms.

May 12, 2024 - The FHA and HUD have revised appraisal rules for FHA single-family loans. The revisions are meant to address issues including housing discrimination at the appraisal level, and provide home buyers with clarified guidelines to contest an appraisal or request a reconsideration of value (ROV).

May 11, 2024 - FHA home loans are just one way to buy a home. Some borrowers pay in cash, some use conventional mortgages, and some qualify for VA home loans. But what do all of these have in common in many cases? The need to use home loan earnest money as part of the transaction.

May 10, 2024 - Which services are required for FHA loans, and which ones are optional? Some borrowers ask this in the planning stages because they’re trying to find ways to stretch their home loan budgets for closing costs and the down payment. We examine some critical services in this article.

May 8, 2024 - You cannot make a down payment or pay closing costs with cold, hard cash. You must render payment in the manner acceptable to the lender, which is typically a wire transfer or some other pre-arranged procedure for down payment money.